Dogecoin started as a playful meme coin back in 2013. It has since become a go-to digital asset for tipping, quick payments, and community projects. Fast blocks and low fees keep it practical for everyday use. In 2026 the coin still draws strength from its loyal community and fresh platform integrations.

Dogecoin runs on its own proof-of-work chain. Blocks arrive roughly every minute, so confirmations feel almost instant for small transfers. There is no hard supply cap; instead the network adds about 5 % new coins each year, though that rate slowly tapers. The design favors spending over long-term hoarding. Community input on forums and social channels shapes upgrades, including recent work on scalability and privacy. People like the lighthearted branding and real uses such as merchant payments. Compared with newer meme tokens, Dogecoin enjoys deeper liquidity and more mature infrastructure, which lowers some risks. Its price still reacts sharply to hype, as past social-media spikes have shown.

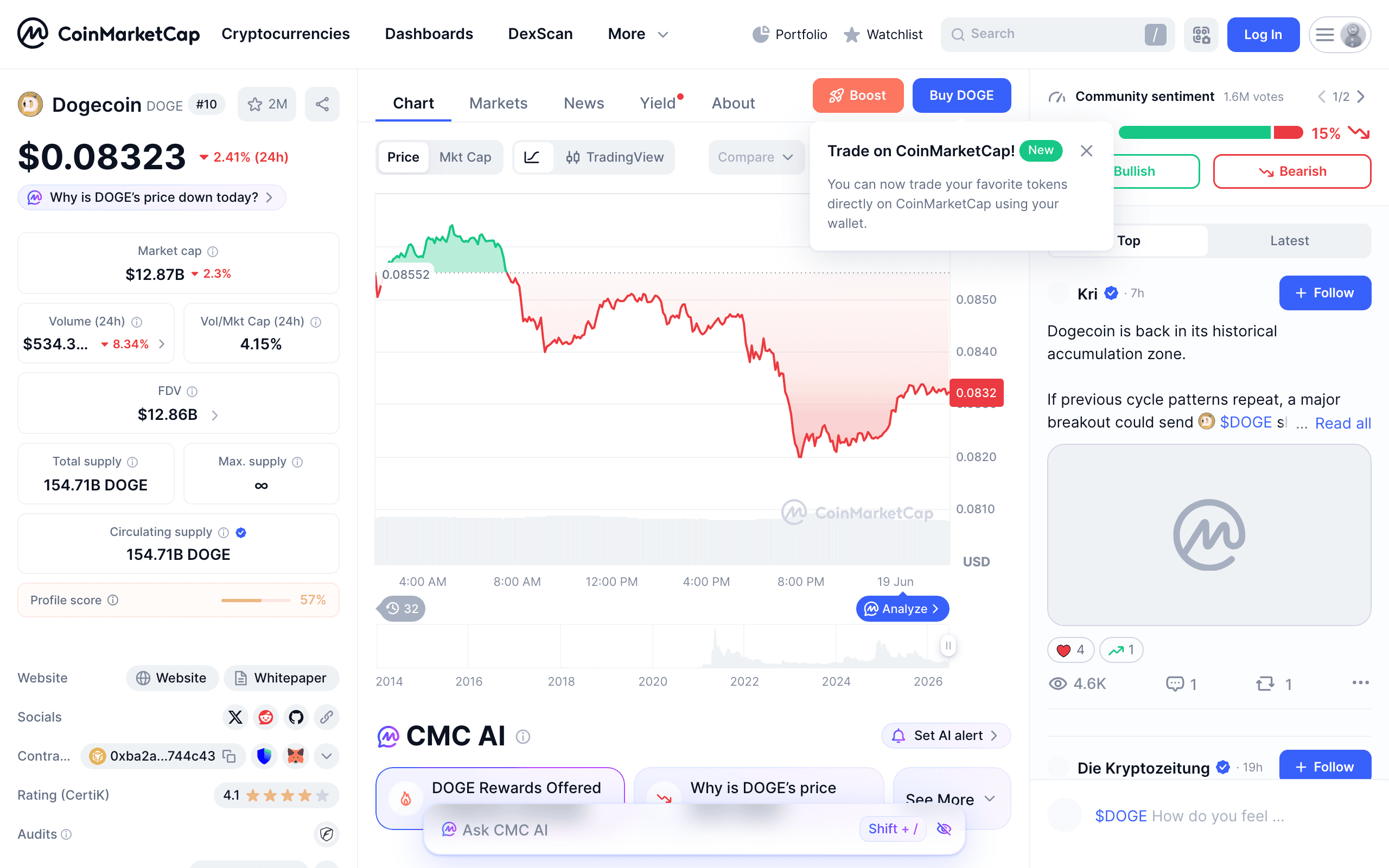

Market cap sits in the mid-billions, keeping Dogecoin inside the top 20 cryptocurrencies. Daily volume hovers in the hundreds of millions across big exchanges, showing steady retail interest. The price has held up through broader swings, helped by wallet upgrades and payment partnerships. Data from CoinMarketCap points to growing use in dApps and cross-chain bridges. Sentiment stays cautiously positive, with analysts watching Bitcoin’s moves and meme-culture trends. Modest institutional interest via futures adds a layer of legitimacy. This backdrop helps frame both buying opportunities and the outlook ahead.

Analysts see 2026 prices ranging from roughly $0.20 on the conservative side to above $0.50 in bullish cases. Growth would come from wider payment adoption and possible ETF inflows. History shows Dogecoin often shines in retail-driven bull runs. Downside risks include tighter rules or shifting attention toward utility tokens. Watch network hash rate and social buzz on X for clues. A steady climb looks plausible if the wider market settles, yet volatility will stay the norm. Long-term holders may benefit from community momentum, while traders track moving averages. Treat every forecast as speculative and do your own research.

Look at fees, security, payment options, and ease of use. Centralized exchanges give easy fiat on-ramps but often ask for verification. Decentralized routes offer more privacy yet can mean higher gas fees. Non-custodial aggregators stand out for fast cross-chain swaps without an account. Check liquidity to keep slippage low on bigger buys. Users in the USA or EU should confirm local rules first. Compare spreads and withdrawal times to control costs. Beginners prefer clean interfaces and guides; power users want API access. Read recent user feedback and audit reports before depositing.

Pick a platform that lists Dogecoin. Sign up if needed and finish any required checks. Send funds via bank, card, or crypto transfer and note the fees. Head to a pair like DOGE/USDT or DOGE/BTC. Choose a market or limit order. Double-check the amount and total cost, then confirm. Move the coins to your own wallet right after the trade. Track the transaction on a block explorer. Some platforms let you set up recurring buys. The whole process usually wraps up in under 30 minutes once everything is ready. Always verify addresses before hitting send.

Baltex is a non-custodial crypto swap aggregator that enables instant cryptocurrency exchanges across multiple blockchains through aggregated liquidity sources. If you already hold USDT or ETH, you can swap straight to Dogecoin on Baltex without creating an account for most trades. Open the interface, pick your input asset and Dogecoin as the output, review the best aggregated rate, and confirm. Routes span 200+ networks and more than 10,000 assets, including Solana and Ethereum. Funds stay in your control the whole time. Baltex runs AML screening on flagged transactions but does not require KYC for standard swaps. The tool works well for quick entries when prices dip.

Store long-term holdings in a hardware wallet. Turn on two-factor authentication everywhere and never share seed phrases. Double-check every URL to dodge phishing clones. Use a VPN on public Wi-Fi and keep software updated. For swaps, confirm the receive address character by character. Larger amounts benefit from multisig setups. Watch for common scams such as fake giveaways on social media. Keep offline backups in separate safe spots. Review your portfolio regularly to stay on top of security.

Small purchases can lose value to fees if you do not check them first. Skipping platform research can land you on shady sites. Weak wallet habits lead to lost coins through hacks or simple errors. Chasing short-term hype often ends in losses. Forgetting tax records invites trouble later. Putting everything into one token raises concentration risk. Rushing a swap without comparing rates creates extra slippage. Start with tiny test transactions to learn the flow before scaling up.

Rules differ by country. Some treat Dogecoin as a commodity; others apply securities laws. In the USA, SEC discussions continue to shape access. Europe’s MiCA rules give clearer guidance for service providers. Make sure any platform you use follows local KYC and reporting requirements. Policy shifts can affect liquidity, so check official sources periodically.

Selling or spending Dogecoin can create taxable events in many places. Track your cost basis and dates carefully. Some regions offer breaks for small trades or long holds. Talk to a local tax advisor for advice tailored to you. Good record-keeping apps make the job easier. Staying compliant avoids audits and penalties.

Dollar-cost averaging spreads buys over time and reduces timing stress. Swing trading suits those comfortable with volatility, while long-term holding aligns with community support. Dogecoin shines for micro-payments and tipping thanks to low fees. It fits inside a diversified portfolio for meme-asset exposure. When stability matters more, Bitcoin or other established coins may serve better. Real examples include paying for online goods where accepted or adding a high-risk slice to a broader allocation. Match any plan to your own goals and risk level.