No-KYC crypto debit cards let you spend cryptocurrency with minimal identity checks. They appeal to anyone who values privacy for subscriptions, online buys, or travel. In 2026, tighter rules mean truly anonymous options are rare. Most providers run some AML screening and set limits to stay compliant. BingCard gives one of the quickest starts with virtual cards ready in minutes.

This guide ranks eight solid choices by issuance speed, supported assets, real-user feedback from forums, and how clearly they explain their limits. Fully anonymous spending is tough because Visa and Mastercard networks demand issuer compliance. Many people combine these cards with privacy-focused swaps first.

Verdict summary: BingCard leads for beginners thanks to speed and low barriers. Kripicard fits high-volume online spenders who want flexible funding. Laso Finance shines for Web3 wallet integration. When limits feel tight or compliance flags pop up, a non-custodial swap aggregator like Baltex can help route funds through privacy assets such as Monero before you load the card.

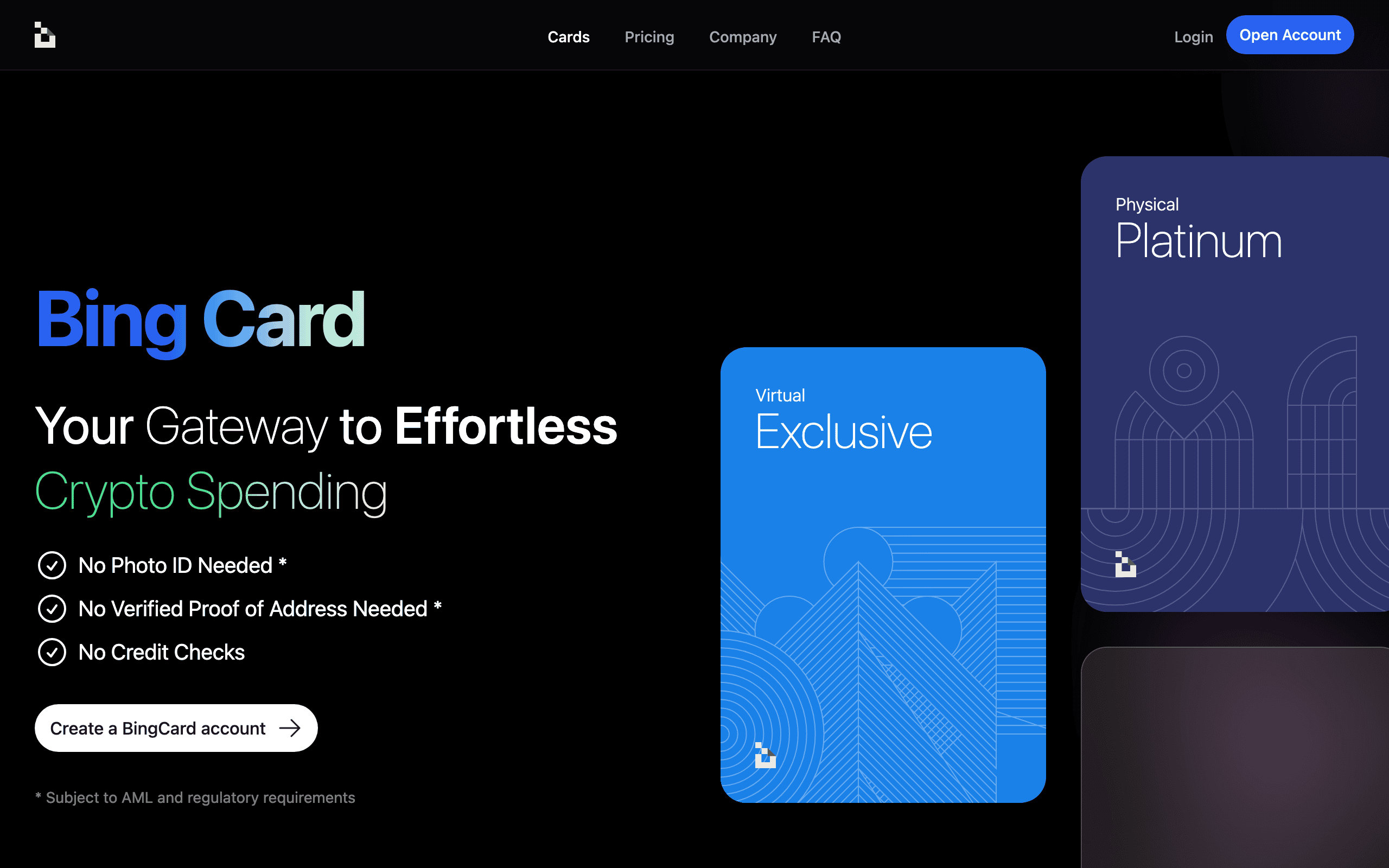

BingCard offers virtual Visa and Mastercard options funded by BTC, USDT, ETH, and USDC. No photo ID or proof of address is needed for basic access, though AML rules still apply. Users report quick setup in under five minutes and reliable online shopping.

Price: Free virtual card with possible reload fees around 1-2%. Key parameters: Supports 150+ assets indirectly, global online acceptance, physical card option available. Rating: 7.5/10.

Why not higher? Real-user complaints on Reddit mention occasional conversion slippage and sudden account reviews that pause spending for days. As of mid-2026, BingCard stays popular for low-stakes anonymous purchases.

Kripicard issues USDT-backed virtual Visa or Mastercard in seconds. Deposits work with USDT, USDC, BTC, ETH, and over 150 other coins. The service stresses no bank account, no credit checks, and no paperwork for initial issuance.

Price: Minimal fees on funding, typically under 1.5%. Key parameters: Works across 90 million merchants, Google Pay and Samsung Pay compatible on select BINs. Rating: 7.2/10.

Why not higher? Some users note daily limits starting at $2,000 that need manual increases, and support can slow during peak hours. It works well for ad payments and subscriptions.

Laso Finance gives a privacy-centric virtual card tied directly to Web3 wallets. Instant issuance happens via wallet signature without personal documents. It focuses on global spending with low personal data exposure.

Price: Free basic tier, premium features at $9 monthly. Key parameters: Supports BTC, ETH, USDT, USDC; Apple Pay and Google Pay ready. Rating: 6.8/10.

Why not higher? Feedback shows lower spending caps around $1,000 monthly and occasional network delays on Ethereum funding. It suits DeFi users who already handle self-custody.

PintoPay offers a simple virtual card with no-KYC onboarding for basic crypto-to-fiat conversion. Setup finishes fast for users who want minimal friction over high limits.

Price: Low or zero monthly fees. Key parameters: Limited asset support focused on major stables; online-only acceptance. Rating: 6.5/10.

Why not higher? Reviews mention higher spreads on conversions and limited customer support documentation. It fits occasional small purchases under $500.

VirPay lets you pick between Visa and Mastercard virtual cards with crypto funding. The platform targets privacy-focused users looking for quick, customizable options.

Price: Competitive reload fees. Key parameters: Broad merchant acceptance, mobile wallet integration. Rating: 6.9/10.

Why not higher? User sentiment on review platforms notes occasional transaction declines and the need for frequent reloads due to conservative limits.

Other notable mentions include services listed on directories like cryptocards.so, which aggregates 16 no-KYC style cards with varying scores. These often share similar traits: instant virtual issuance, crypto funding, and regulatory caps. Physical cards show up less often in true no-KYC flows.

The process starts with connecting a wallet or depositing crypto to the provider platform. The card is generated virtually, funded in real time, and used wherever Visa or Mastercard is accepted. Behind the scenes, the issuer converts crypto to fiat at the point of sale. Privacy comes from skipping traditional ID upload, yet on-chain data and AML screening can still link activity.

Practical example: A user swaps ETH to USDT on a non-custodial platform, then loads BingCard for a $300 online purchase. The transaction settles in fiat without exposing wallet history directly to the merchant.

MiCA in Europe, evolving U.S. rules, and card network policies mean no provider can promise zero compliance checks. Fully anonymous cards that survive long-term are rare. Many services flagged in 2025 reviews have added light verification or reduced limits. Always verify current terms, as offerings change quickly.

These cards suit online shopping, subscription services, gaming top-ups, and travel bookings where cash or bank transfers are undesirable. They fit users already holding crypto who want one-step spending without full exchange KYC.

They are not ideal for high-volume merchants, frequent international travel requiring physical cards, or anyone needing guaranteed high limits. In those cases, compliant self-custodial alternatives with light KYC often provide better reliability and higher ceilings.

Start with major networks like Ethereum, Solana, or Tron for low fees. Convert volatile assets to stables first. Services supporting Monero routing add an extra layer before card funding. Baltex, a non-custodial crypto swap aggregator, enables instant cross-chain exchanges across 200+ networks and 10,000+ assets without registration for most swaps, helping users prepare privacy-oriented funds.

Never store large balances on the card itself. Use unique card details per merchant when possible. Monitor for AML flags that can freeze funds. Combine with hardware wallets for cold storage of reserves. Test small amounts first.

All share the trade-off of capped spending versus full anonymity.

Selection prioritized real availability in 2026, documented no-KYC flows, user reports from Reddit and review sites, supported assets, and transparency on limits. We weighted issuance speed highest, followed by fee structure and merchant acceptance. Only providers with active websites and recent mentions were included.

Evaluate your typical spend amount, preferred assets, and tolerance for potential reviews. Check supported networks for funding costs. Review recent user experiences for uptime and support quality. Understand that “no-KYC” does not equal “untraceable.”

Use privacy coins or mixers only where legal. Keep records of swaps for personal tax purposes. Avoid sharing card details publicly. Stay updated on regulatory shifts that could affect service availability.

As regulations evolve, expect more hybrid models blending light verification with self-custody features. Non-custodial infrastructure will remain key for preparing funds privately before any card load.

G. Khan

G. Khan

G. Khan

G. Khan

G. Khan

G. Khan